Key Takeaways

- When a patient opens their insurer’s app and speaks to a virtual GP, they have already crossed a boundary — from NHS constitutional domain into a commercial pathway. The crossing is invisible because it looks like a consultation.

- The digital front door creates a one-way valve: smooth entry into the insured pathway, ungoverned exit back to the NHS. Virtual GPs cannot refer via the NHS e-Referral Service.

- Clinical data enters commercial infrastructure at the first interaction — processed for both clinical and commercial purposes, under consent architecture established through terms and conditions, not informed consent during the consultation.

- Symptom checkers are clinical service routers, not search engines. When an algorithm decides ‘book a physio’ rather than ‘see a GP urgently,’ it is practising a form of clinical triage with material liability.

- The digital-physical handover loses clinical context: the virtual GP’s full clinical narrative rarely reaches the physical specialist, who starts the assessment from scratch with a referral letter.

This is the fifth article in a series examining boundary governance in private healthcare. The first four articles established that private healthcare governs individual organisations while leaving the crossings between them unaudited, that insurer provider networks govern financial flows at every boundary while leaving clinical flows ungoverned, that the clinical-commercial boundary at pre-authorisation has no regulatory home, and that the NHS-private interface — the boundary every insured patient crosses at least twice — connects two constitutional domains with no governed crossing mechanism. This article examines the boundary that most patients do not recognise as a boundary at all: the digital front door.

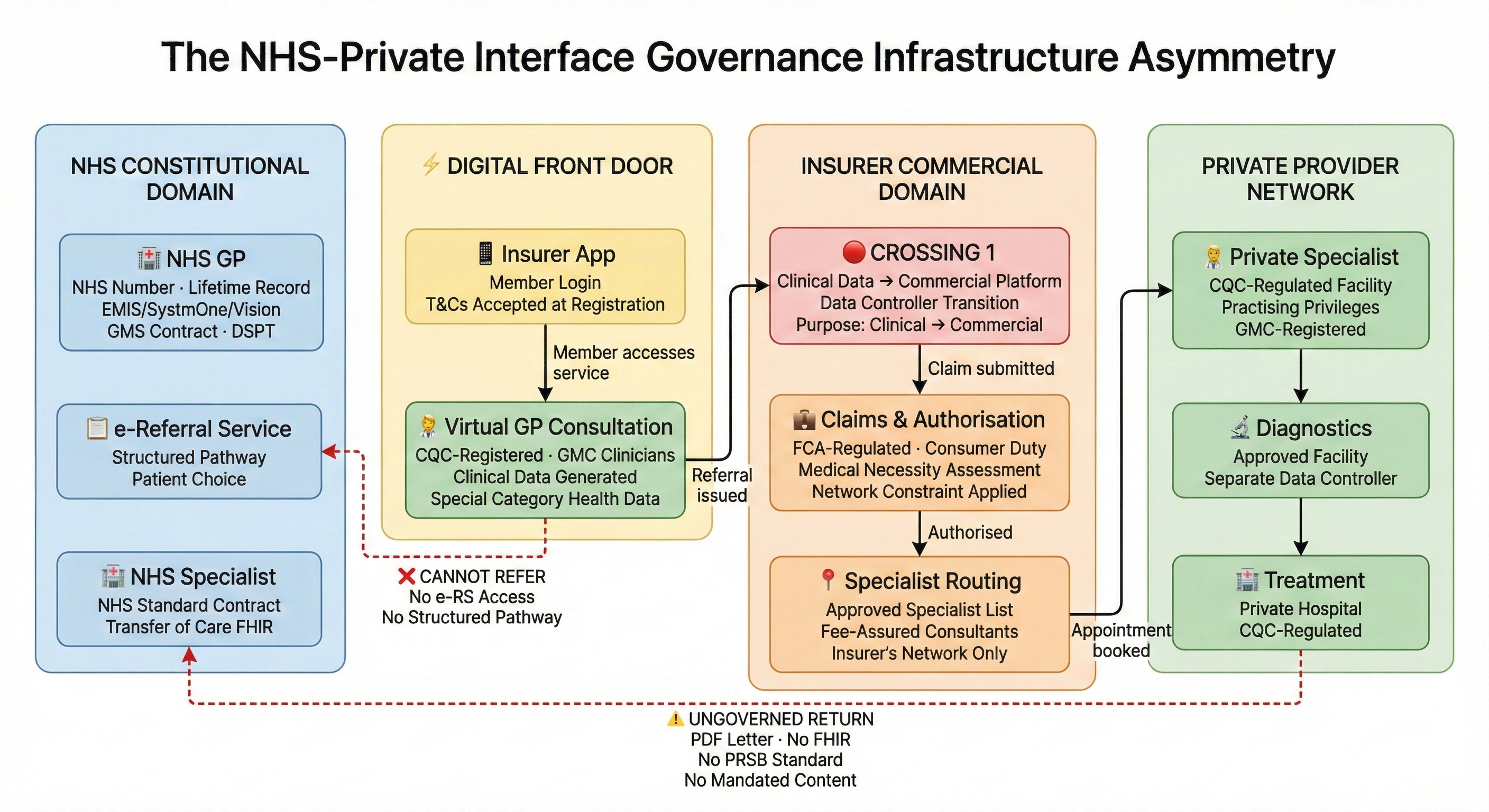

When a patient calls their NHS GP surgery, they are inside the NHS constitutional domain from the first word. The clinical record is NHS. The data governance framework is NHS. The referral pathway — if one is needed — runs through the NHS e-Referral Service to NHS or NHS-contracted providers. The patient knows where they are.

When a patient opens their insurer's app and speaks to a virtual GP, they have already crossed a boundary. They may not know it. The interface looks like a GP consultation. The clinician is GMC-registered, experienced, trained specifically in virtual consultation. The service is CQC-registered. The patient receives a diagnosis, a prescription, clinical advice. Everything about the experience says: this is healthcare.

It is healthcare. It is also a commercial pathway. The clinical data generated in that consultation enters a commercial platform. The routing decision — where this patient goes next — is made inside the insurer's ecosystem. The referral, if one is issued, goes directly to the insurer's claims and authorisation function, not to the NHS. Everything that follows in the patient's insured journey is shaped by what happens at this first crossing. And it is the least examined boundary in private healthcare, because it does not look like a boundary. It looks like a consultation.

The structural pattern

Every major UK private medical insurer now includes a virtual GP service as a standard benefit. The pattern is consistent. AXA Health offers Doctor at Hand, powered by Doctor Care Anywhere, providing 24/7 access to GPs and Advanced Clinical Practitioners who can assess, diagnose, prescribe, and — critically — refer directly into the insurer's specialist network. Bupa's Digital GP service operates on the same model: same-day consultations, referrals flowing into Bupa's authorisation and specialist booking pathway. Vitality integrates its GP service with its broader wellness and rewards programme. Aviva positions its Digital GP app as the member's “first port of call” for non-emergency concerns.

The services differ in detail. They share a structural architecture. A clinical consultation is delivered by a CQC-registered provider, using GMC-registered clinicians, through a platform either owned by, contracted to, or white-labelled for the insurer. When the consultation results in a referral, the referral enters the insurer's commercial pathway: claim authorisation, specialist selection from the insurer's approved list, appointment booking through the insurer's service team. AXA's “Fast Track Appointments” team, for example, typically finds a specialist slot within 48 hours of the Doctor at Hand GP providing a referral.

This is marketed — reasonably — as speed and convenience. A patient can consult a GP within hours rather than waiting days or weeks for an NHS appointment. The referral is digital and immediate rather than requiring a letter, a phone call, or a physical visit to a surgery. The pathway from symptom to specialist can be measured in days rather than months. In the context of NHS waiting lists exceeding 7.5 million treatment pathways, the value proposition is real.

The governance question is not about the clinical quality of the consultation. It is about what happens at the edges of it.

The first crossing: clinical data enters commercial infrastructure

The patient's first interaction with the virtual GP generates clinical data. Symptoms described, history taken, examination findings recorded, clinical reasoning documented. Under UK GDPR, this is special category data — health data whose processing requires both an Article 6 lawful basis and an Article 9 condition. The ICO has been explicit that for special category data, explicit consent must be “freely given, specific, affirmative and unambiguous” and that the consent lawful basis is “rarely appropriate in the context of health and social care information.”

The virtual GP service is a data controller. The insurer is a separate legal entity — either a separate data controller, or a joint controller, depending on the contractual architecture between the clinical service provider and the insurer. When the virtual GP refers the patient to a specialist, clinical data crosses from one controller to another. When the insurer's authorisation team reviews the referral to determine whether the treatment is covered and whether the provider is approved, clinical data is being processed for a commercial purpose by an FCA-regulated entity operating under a financial services governance framework.

The patient consented to a clinical consultation. But what exactly did the patient consent to at the point of data processing? Did they understand that their clinical data would flow from the GP consultation into the insurer's commercial infrastructure? That it would inform routing decisions — which specialist, which facility, which pathway? That it would be processed for claims authorisation by the insurer's clinical team, whose role was examined in the third article in this series? That elements of their clinical data might be retained for quality metrics, utilisation analysis, or product design?

The consent architecture at the digital front door is typically established through terms and conditions accepted before the first consultation — a contractual consent mechanism, not the informed consent to specific data sharing given during a clinical interaction. The ICO's guidance on transparency in health and social care, published in April 2024, specifically highlighted that organisations increasingly use health data for purposes beyond direct care — service planning, research, collaboration with partners — and that these additional uses require additional explanation. The digital front door, by design, uses clinical data for both clinical and commercial purposes from the very first interaction. Whether the consent architecture adequately reflects this dual purpose is a question that most virtual GP services have addressed through privacy policies rather than through the clinical consultation itself.

The Data (Use and Access) Act 2025, which received Royal Assent in June 2025, introduces mandatory information standards for IT suppliers to the NHS and lays the groundwork for smart data schemes in health — secure systems allowing patients to share health records with approved third parties. The Act clarifies that organisations cannot rely on another body's statutory functions to legitimise their own data processing. For insurer-integrated virtual GP platforms, this clarification matters: the virtual GP service's lawful basis for processing health data for clinical purposes does not automatically extend to the insurer's processing of the same data for commercial purposes. Each controller must independently establish its own lawful basis and Article 9 condition.

The one-way valve

The structural consequence of the digital front door is directional. The virtual GP integrated with an insurer's pathway can refer into the insurer's specialist network — instantly, digitally, within the same platform. The insurer's authorisation team can process the referral within hours. The specialist appointment can be booked within days. The pathway flows smoothly in one direction: into the insured ecosystem.

It cannot flow in the other direction. The virtual GP cannot refer to the NHS.

The Private GP Forum states this plainly: private practitioners in the UK do not have access to the NHS e-Referral Service. For urgent referrals — suspected cancer requiring a two-week-wait pathway, for instance — the private GP must contact the local cancer referral team directly, typically through NHS Mail or a secure email platform. For routine referrals, the private GP must either liaise with NHS departments directly or provide consultation notes for the patient to take to their NHS GP, who can then make the referral through the e-Referral Service.

This is not a minor administrative inconvenience. It is a structural asymmetry with clinical consequences.

Consider a patient who enters through the digital front door with symptoms that could indicate either a condition treatable within the insurer's specialist network or a condition requiring NHS-only services — complex cancer pathways, tertiary neurosurgery, specialist mental health crisis teams, or services simply not covered by the patient's policy. The virtual GP cannot route the patient to NHS services through the same seamless digital pathway available for insured care. The patient must re-present to their NHS GP and start again. The fourth article in this series documented what that return crossing looks like: no structured referral mechanism, no mandated content standard, clinical information carried in a PDF letter or not at all, clinical responsibility sitting in a gap between the private clinician who discharged and the NHS GP who has not yet accepted.

The digital front door creates the first crossing in the insured pathway. It also determines whether the patient has access to the full healthcare system, or only to the commercial subset of it. For most conditions, the insured pathway works. For the conditions where it does not — where the patient needs services the insurer does not cover, where benefit limits are exhausted, where the clinical situation escalates beyond what the private network can provide — the patient faces a boundary crossing back to the NHS that has no governed mechanism. The ease of entering the insured pathway through the digital front door is not matched by any equivalent ease of returning to the NHS when the insured pathway cannot deliver what the patient needs.

This is the one-way valve. Smooth entry. Ungoverned exit.

The CQC assesses the consultation, not the crossing

Virtual GP services are CQC-registered. The clinicians are GMC-registered. The consultation itself — the ten or fifteen minutes in which a patient describes symptoms and a clinician assesses them — is clinically governed. The CQC can inspect the service and assess whether the consultations are safe, effective, caring, responsive, and well-led.

But the CQC's remit ends at the edge of the clinical service. The crossing from the consultation to the insurer's routing function — the moment where clinical data leaves the CQC-regulated domain and enters the FCA-regulated domain — is outside CQC's regulatory scope. The insurer's decision about which specialist to authorise, which facility to direct the patient to, whether to approve the virtual GP's recommended investigation or propose an alternative — these are commercial decisions with clinical consequences, made by an entity the CQC does not regulate.

The digital front door is a well-regulated node connected to ungoverned edges. This is the same pattern identified across every boundary in this series. But the digital front door adds a complication: the node and the edge are often operated by the same commercial entity, or by closely integrated entities. When the virtual GP service is owned by, contracted to, or white-labelled for the insurer, the boundary between clinical service and commercial pathway may be architecturally invisible. The patient's experience is seamless. The governance transition is undetectable.

The NHS Digital Technology Assessment Criteria (DTAC) — the national baseline for digital health technologies entering the NHS — requires compliance with DCB 0129 (clinical safety for manufacturers), data protection standards, technical security, interoperability, and usability. DTAC applies to technologies entering the NHS ecosystem. A virtual GP platform operating purely in the private sector, serving insurer members rather than NHS patients, does not need to demonstrate DTAC compliance. No private sector equivalent of DTAC exists. No clinical safety standard equivalent to DCB 0129 is mandated for the insurer's routing platform, the pre-authorisation decision engine, or the clinical-to-commercial data crossing at the digital front door.

The consultation is regulated. The platform is regulated. The crossing between them — where clinical data becomes commercial data, where a clinical recommendation becomes an authorisation request, where a patient becomes a claim — has no regulatory framework specific to it.

The app as Service Router: when algorithms direct care

Before the patient reaches a virtual GP, they often interact with something else first: a symptom checker. Bupa, AXA, Vitality and Aviva all offer in-app triage tools that assess symptoms and direct the member to the appropriate service — self-care advice, a pharmacist, a virtual GP consultation, or A&E. These tools are not search engines. They are clinical decision support systems performing Service Routing (Flow #6). When an algorithm decides “book a physio” rather than “see a GP urgently,” it is practising a form of clinical triage. The routing decision has clinical consequences.

The commercial conflict is structural. Insurers are investing in “digital first” strategies explicitly to reduce claims costs — deflecting GP visits, managing demand through self-care pathways, routing to lower-cost interventions where clinically appropriate. This is legitimate. But it creates a tension between commercial triage (cheapest clinically acceptable route) and clinical triage (safest route regardless of cost). If the algorithm is weighted — by design or by training data — to route patients toward lower-cost providers (physiotherapy, pharmacy) rather than higher-cost investigations (MRI, specialist referral), that weighting is a clinical decision embedded in commercial logic. And if the algorithm misinterprets “chest pain” as musculoskeletal when it is cardiac, the app owner — the insurer — holds liability for the patient safety incident. The app is not a channel. It is a clinical service router with material liability attached.

The “black box” hazard: governance in AI triage

AI-powered symptom checkers introduce a governance problem that traditional clinical services do not face: the reasoning is opaque. A human GP can explain why they referred a patient urgently. A neural network that classifies symptom clusters against training data cannot explain its reasoning in terms that a clinical governance framework can audit. The app captures keywords — “headache” — but may miss clinical intent: “headache after a fall” is a fundamentally different clinical presentation from “headache with stress.” The difference between the two may be a subdural haematoma.

The governance response is not to avoid AI. It is to apply clinical safety methodology to algorithmic pathways. DCB 0129 — the clinical risk management standard for health IT — requires manufacturers to maintain a Clinical Safety Case and a Hazard Log. Every algorithmic routing decision is a potential hazard: a failure to escalate, a misclassification, a routing to a service that cannot address the patient's actual condition. Each pathway through the triage algorithm should be risk-assessed for failure modes, with defined mitigations. The question is not whether the algorithm is accurate on average. The question is what happens at the edges — the cases where the algorithm's confidence is low, where the symptom presentation is ambiguous, where the routing decision could be the difference between timely intervention and missed pathology. The Hazard Log should capture these edge cases explicitly.

The digital-physical handover: where data dies

The virtual GP consultation generates a clinical record. The record sits on the virtual GP platform's clinical system — Doctor Care Anywhere, eMed, or whichever provider powers the insurer's service. When the virtual GP refers the patient to a physical specialist, the clinical narrative must cross from the virtual platform to the specialist's practice or the private hospital's EHR. In most cases, it does not cross cleanly.

The virtual GP platform operates on a separate technology stack from the insurer's main system, which in turn is separate from the hospital's EHR (InHealth, Compucare, or a bespoke system). The referral generates a document — typically a PDF or a structured message into the insurer's authorisation system — but the full clinical narrative, the consultation recording, the clinical reasoning that led to the referral, the symptoms described and the examination findings noted, may not transfer. The patient arrives at the physical specialist appointment with a referral letter. The specialist starts the clinical assessment substantially from scratch. This is a Provenance (Flow #3) failure: the clinical information exists, but its origin, context, and completeness are lost at the crossing between virtual and physical care.

The consequence is duplication (repeated investigations, wasted cost, delayed diagnosis) or risk (acting on incomplete information without knowing it is incomplete). The digital front door promises seamless access. The digital-physical handover delivers fragmentation — and the patient, who experienced what felt like a continuous pathway, does not know that their clinical history was lost at the boundary between two technology platforms that were never designed to interoperate.

Software as a Medical Device: the regulatory trap

The MHRA's guidance on medical device software is clear in principle: if software has a medical purpose — diagnosis, prevention, monitoring, treatment, or alleviation of disease — it is a medical device under the UK Medical Devices Regulations 2002 (as amended). Software that provides a diagnosis or recommends a treatment pathway meets this definition. Software that merely provides general health information does not.

The digital front door sits in the gap between these two definitions. Marketing says: “Diagnose your symptoms!” Legal says: “For information only.” The app presents itself to the user as a clinical tool — enter your symptoms, receive a recommendation, book a consultation. The terms and conditions present it to the regulator as an information service — not a diagnostic tool, not a substitute for professional medical advice. If it looks like a clinical decision support system and the patient relies on it as one, the disclaimer may not protect the operator when the MHRA investigates a patient safety incident.

The MHRA has already signalled its direction. Its concerns about Babylon Health specifically highlighted a “legal gap” around triage chatbots — software that directs patients to services based on symptom assessment but claims not to be a medical device. The regulatory trap is closing. Insurers and healthtech companies that classify their triage tools as information services to avoid MHRA regulation are building on a foundation that the regulator is actively undermining. The prudent approach is to assume the tool is a medical device, apply DCB 0129 clinical safety methodology regardless of current classification, and maintain a Hazard Log that documents the clinical risks of every routing pathway. The cost of compliance is modest. The cost of an MHRA investigation following a patient safety incident in which the tool was classified as “information only” is reputational, regulatory, and potentially existential.

The consolidating market

The virtual GP market serving UK private medical insurers is consolidating rapidly. Doctor Care Anywhere powers AXA Health's Doctor at Hand service and provides virtual GP services under white-label arrangements to multiple insurance and corporate clients. eMed Healthcare UK, which acquired the UK operations of Babylon Health out of administration in August 2023, provides digital-first primary care to both NHS patients (through the GP at Hand service) and private patients through insurer partnerships including Bupa, Aviva, and Freedom Health Insurance.

Babylon's trajectory is instructive. Once valued at approximately $4.2 billion, the company collapsed in 2023 following years of controversy: a data breach in which patients could view other patients' consultation recordings, MHRA concerns about the safety of its AI-powered symptom checker, ASA rulings that its advertising misled patients about the requirement to deregister from their existing GP, and sustained criticism from the profession that the service cherry-picked younger, healthier patients while destabilising the funding of local GP practices. The UK operations were sold for approximately £500,000.

What is significant about the Babylon story is not the corporate failure. It is that the infrastructure survived. The clinical service, the technology platform, the insurer contracts, the patient relationships — all transferred to a new owner. The digital front door continued operating. The governance questions that surrounded Babylon — about data governance, about the boundary between clinical service and commercial platform, about the MHRA's assessment that the regulatory regime did not adequately cover software-powered health tech devices — transferred with it.

Market consolidation means a small number of platforms increasingly power the digital front door for multiple insurers. The same clinical consultation infrastructure, the same data processing architecture, the same boundary between clinical and commercial domains, replicated across insurer brands. The governance question is not brand-specific. It is architectural.

Consumer Duty and the designed pathway

The FCA's Consumer Duty, fully in force and a priority focus area for 2025–26, requires insurers to deliver good outcomes for customers across four dimensions: products and services, price and value, consumer understanding, and consumer support. The FCA has committed to consulting on how the Duty applies through distribution chains and is working with the ICO on the interaction between Consumer Duty requirements and data protection expectations, with joint guidance expected in Q1 2026.

The digital front door sits squarely in this intersection. The insurer designed the product. The product includes the virtual GP service. The virtual GP service generates the referral. The referral enters the insurer's authorisation pathway. The pathway directs the patient through the insurer's provider network. The outcome — clinical and commercial — is a direct consequence of the pathway the insurer designed.

Under the Consumer Duty's products and services outcome, the insurer must ensure the product is designed to meet the needs of the target market. If the digital front door channels patients into an insured pathway that cannot serve them when their condition requires NHS-only services, when their benefit limits are exhausted, or when the provider network lacks the appropriate specialist — the product has a foreseeable limitation that the insurer must have considered and addressed.

Under the consumer understanding outcome, the patient must receive information that enables them to make informed decisions. Does the patient entering through the digital front door understand that the virtual GP can refer them into the insurer's network but cannot refer them to the NHS? Do they understand that their clinical data will be processed by the insurer for commercial purposes? Do they understand that the “open referral” issued by the virtual GP directs them to the insurer's approved specialist list, not to the full range of specialists available to an NHS patient?

Under the consumer support outcome, the insurer must ensure that customers can pursue their interests without unreasonable barriers. When a patient needs to exit the insured pathway and return to NHS care, the absence of a governed crossing mechanism is, structurally, a barrier — not one the insurer necessarily created, but one the insurer's product design must account for.

The FCA's upcoming consultation on distribution chains will examine how responsibility flows between entities in the chain. The digital front door is a distribution chain: the insurer (product manufacturer) contracts with a virtual GP platform (service provider) which refers into a specialist network (care delivery). Clinical data, clinical decisions, and clinical responsibility flow through this chain. The Consumer Duty asks: who is accountable for outcomes at each link?

The governance opportunity

The digital front door is not inherently ungovernable. It is currently ungoverned. The distinction matters.

A virtual GP service that can demonstrate governed boundaries — where clinical data crosses from clinical to commercial domains under explicit, informed, specific consent rather than blanket contractual terms; where clinical intent is preserved as a referral moves from the consultation to the authorisation function; where clinical responsibility is explicitly transferred rather than assumed; where the one-way valve is acknowledged and the exit pathway back to NHS care is defined rather than improvised — is a service that can demonstrate Consumer Duty compliance in ways its competitors cannot.

A virtual GP platform that can show regulators — CQC assessing the clinical service, FCA assessing the insurer, ICO assessing data governance — that the boundary between clinical and commercial processing is architecturally defined, not just contractually declared, occupies a different regulatory position from a platform where the boundary is invisible. This is the infrastructure that governance-preserving interoperability is designed to provide.

The organisations operating the digital front door are not lacking clinical quality. The consultations are CQC-inspected. The clinicians are experienced. The technology is functional. What is lacking is governance of the edges — the crossings between the clinical consultation and the commercial pathway, between the insurer's ecosystem and the NHS, between the data controller processing health data for clinical purposes and the data controller processing it for commercial ones.

The Seven Flows at the digital front door

Can the organisations operating the digital front door demonstrate, at each boundary crossing, that seven governance questions are addressed?

Identity. The virtual GP verifies the patient's identity against the platform's registration. The insurer verifies the patient's identity against their policy. The patient's NHS GP holds their identity verified against the NHS Personal Demographics Service, linked to their NHS number and lifetime clinical record. These are three separate identity assertions maintained by three separate organisations. When clinical information generated by the virtual GP is transmitted to the patient's NHS GP — as several services offer — how is the identity reconciliation between the platform's patient record and the GP's patient record assured? Is the NHS number used as the definitive identifier, or does reconciliation depend on someone correctly matching a name on a letter to a patient in a clinical system?

Consent. The patient consented to a clinical consultation. Did the patient give explicit, specific, informed consent to their health data being shared with the insurer's commercial function for authorisation purposes? Did they consent to their clinical data informing the insurer's routing decision? Was this consent established during the clinical interaction — as informed consent to a specific data sharing event — or through terms and conditions accepted at registration, potentially months earlier? The ICO's position that consent is “rarely appropriate” for health and social care data processing raises the question of what alternative lawful basis and Article 9 condition each controller in the chain is relying upon, and whether this is transparent to the patient.

Provenance. Clinical information generated in the virtual GP consultation carries the provenance of a CQC-registered clinical service. When that information crosses into the insurer's authorisation system, does the provenance travel with it? When the insurer's authorisation team reviews the referral, do they know — and does their governance framework require them to know — the clinical context in which the information was generated? When the referral reaches the specialist, does the specialist know the information originated from a ten-minute virtual consultation rather than a face-to-face examination with access to the patient's full NHS medical record?

Clinical Intent. The virtual GP's clinical reasoning — their assessment of what the patient needs and why — must survive the crossing from consultation to authorisation. Pre-authorisation forms capture diagnosis codes and procedure requests. They rarely capture the nuanced clinical reasoning that led to the referral: why this investigation rather than that one, what differential diagnoses are being considered, what the virtual GP could and could not assess in a remote consultation. If the insurer's authorisation team substitutes a different investigation or directs the patient to a different specialist, are they doing so with full knowledge of the virtual GP's clinical intent?

Responsibility. The virtual GP holds clinical responsibility during the consultation. At what point does that responsibility transfer? When the referral is submitted to the insurer? When the insurer authorises it? When the specialist accepts the patient? If the insurer declines the referral or modifies it — authorising a different investigation, directing the patient to a different specialist — who holds clinical responsibility for the clinical consequences of that modification? The virtual GP recommended one course of action. The insurer's commercial process produced a different one. The patient proceeded on the insurer's pathway. If the outcome is poor, the responsibility gap identified in the third article of this series begins at the digital front door.

Service Routing. The virtual GP's referral routes the patient into the insurer's provider network — the approved specialist list, the recognised facilities, the fee-assured consultants. This routing is based on the insurer's network design. Is the routing clinically appropriate, or is it constrained by which specialists have agreed to the insurer's fee schedule? If the patient's condition requires a specialist not on the approved list, or a facility outside the network, does the digital front door platform have a mechanism for routing outside the insured pathway? Or does the one-way valve apply: smooth routing into the network, no structured routing out of it?

Outcome. Does the virtual GP service know what happened after the referral? Did the specialist agree with the virtual GP's assessment? Was the treatment effective? Were there complications? Did the patient end up back with their NHS GP with a problem the insured pathway could not resolve? The outcome loop — the feedback that closes the clinical cycle — would need to cross back from the specialist, through the insurer's pathway, to the virtual GP platform. There is no structured mechanism for this. The digital front door opens onto a pathway. It does not know where the pathway leads.

The digital front door is the most successful innovation in UK private healthcare access in recent years. It has reduced waiting times, improved convenience, and put a GP consultation within hours rather than weeks. It has also created the least visible boundary in the private healthcare system — a crossing where clinical care becomes a commercial pathway, where health data enters a commercial platform, and where the patient's access to the full healthcare system narrows to the insurer's network. The organisations that govern this boundary — that make the crossing visible, auditable, and safe — will define the next generation of digital healthcare. The organisations that do not will find that the CQC, the FCA, and the ICO are each, from different directions, asking the same question: what happens at the edge of the consultation?

Next in the series: Clinical safety at private healthcare boundaries — what happens when DCB 0129 does not reach the crossings where clinical risk is highest.

Private Healthcare Governance Series

- #1 Practising Privileges and the Governance Gap

- #2 The Provider Network as Ungoverned Constellation

- #3 The Clinical-Commercial Boundary

- #4 The NHS-Private Interface

- #5 The Digital Front Door (this article)

- #6 Clinical Safety at Boundaries

- #7 The Seven Flows Applied to Insured Pathways

- #8 The Regulatory Convergence

Related: Architecting Neighbourhood Health

The same boundary governance methodology applied to NHS multi-organisation networks — including the constitutional complexity of co-locating five independent organisations in a single building.

Sources and further reading

- AXA Doctor at Hand — Doctor Care Anywhere

- NHS e-Referral Service — NHS England Digital

- Private GP Forum — Do private practitioners have access to the e-Referral Service?

- ICO — Special category data conditions for processing

- ICO guidance on transparency in health and social care (Navigator Law summary)

- Data (Use and Access) Act 2025 — GOV.UK overview

- Data (Use and Access) Act 2025 — health sector perspective

- Digital Technology Assessment Criteria (DTAC) — NHS England

- CQC operational effectiveness review — Dr Penny Dash (GOV.UK)

- FCA Consumer Duty focus areas 2025–26

- FCA Consumer Duty — distribution chains consultation (Ashurst summary)

- FCA/ICO joint work on Consumer Duty and data protection

- Babylon Health — Wikipedia

- eMed Healthcare UK acquires Babylon

- Former Babylon UK chief appointed CEO at Doctor Care Anywhere

- MHRA concerns about Babylon Health (TechCrunch)

- Babylon GP at Hand adverts banned by ASA (Pulse Today)

- Digital health apps and telemedicine in the UK (CMS Expert Guide)

- GP training: what to do when a patient wants a private referral (GPonline/MDU)

- NHS England — mandatory information standards and Data (Use and Access) Act