Key Takeaways

- Leading PMI insurers have built genuinely impressive pre-episode prevention models — but their data and intelligence stop at the practice door, exactly where Consumer Duty evidence is needed most.

- The FCA’s multi-firm review found most insurers lack direct evidence of what customers actually experience at the claims stage. Population health data does not answer individual episode questions.

- AI-enabled care pathway ambitions require structured data from inside care pathways — data that no PMI insurer currently captures at the point of inter-organisation handover.

- The Paterson Inquiry and Consumer Duty ask the same question from opposite directions: what happened inside the funded episode? The current PMI architecture cannot answer either.

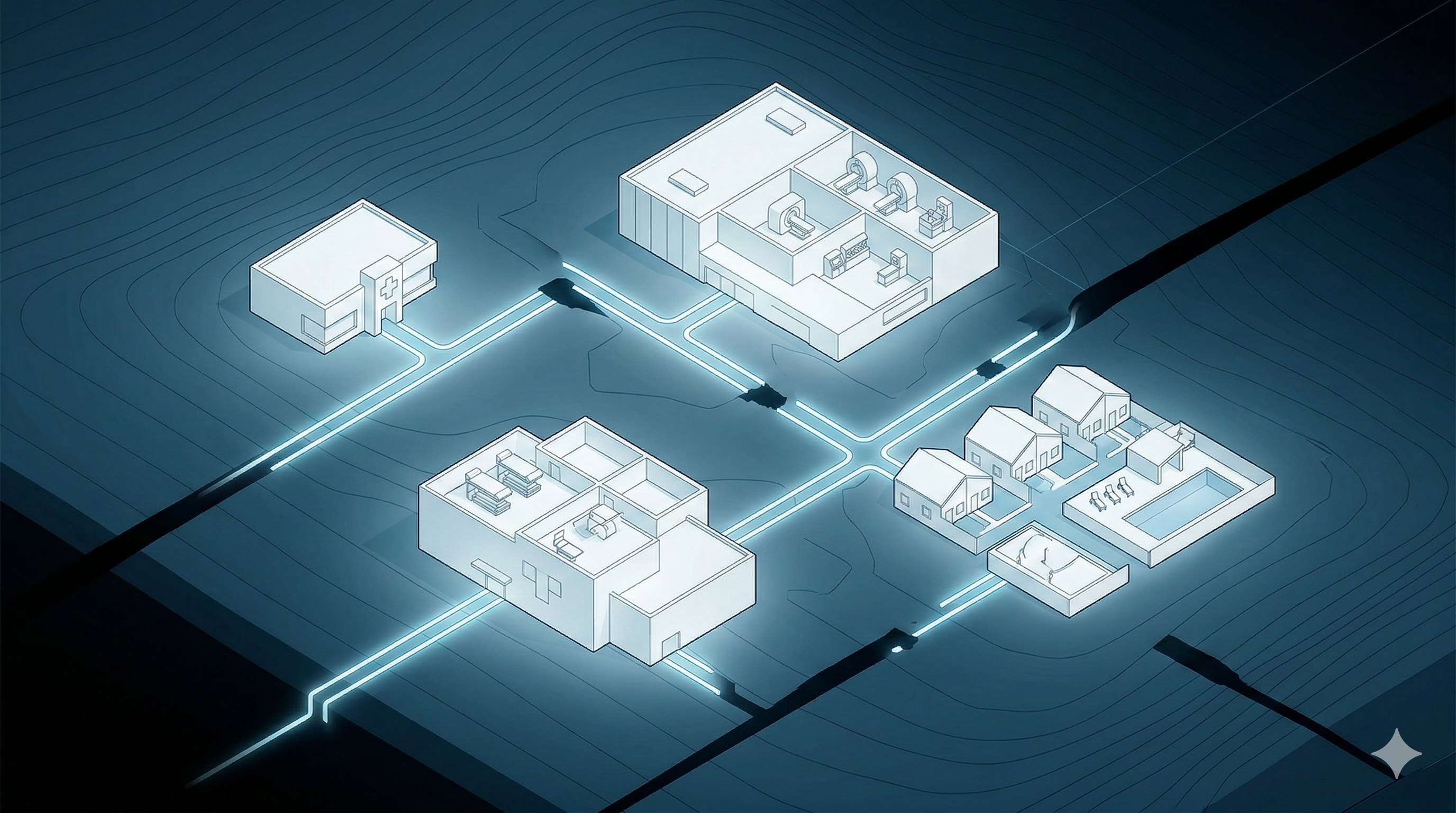

- The Seven Flows framework — Identity, Consent, Provenance, Clinical Intent, Alert and Responsibility, Service Routing, and Outcome — extends the prevention model into the episode, producing the evidence both regulators require.

- The first insurer to close the episode gap holds a measurable competitive position at FCA review, employer renewal, broker market, and FOS disputes that cannot be replicated through product innovation alone.

The private medical insurance market has, in the last three years, produced something genuinely impressive. Driven by the requirements of Consumer Duty and accelerated by mounting NHS pressure, the leading insurers have rebuilt their proposition around a compelling new thesis: that the highest value a health insurer can deliver is not a claim paid quickly, but an illness prevented entirely.

Vitality calls this Prevention 2.0. The concept is well-evidenced, commercially coherent, and meaningfully different from the indemnity-first model that defined PMI for most of its history. Their peer-reviewed study of 465,000 members, conducted over seven years with the London School of Economics, found that members who moved from inactive to active lifestyles reduced their mortality risk by up to 57% — equivalent to five additional years of life expectancy. Their 2026 PMI predictions name AI-enabled care pathways and upstream prevention as the defining forces shaping the next era of private healthcare. Their Google AI partnership, announced as a seminal development for the year, extends the intelligence model further into personalised health management and genomic risk profiling.

This is the most sophisticated pre-episode health intelligence model in UK insurance. It deserves to be recognised as such.

It also stops, without exception, at the practice door.

What Consumer Duty Is Actually Asking

The FCA’s Consumer Duty came into force in July 2023 and has been tightening its expectations ever since. Its multi-firm review of insurance outcomes monitoring, conducted across 20 large insurers and updated in December 2025, found that most firms “rely on process-based MI and lack direct evidence of what customers actually experience, especially at the claims stage.”

The regulator was specific about what constitutes poor practice: monitoring focused on process completion rather than outcomes delivered, data that does not facilitate scrutiny or challenge, and the assumption that completing a product review automatically indicates good outcomes were achieved. It was equally specific about what good practice looks like — combining a wide range of metrics, mapping testing to actual customer journeys, and being able to demonstrate that improvements in outcomes were delivered in response to identified poor outcomes.

For 2026, the FCA has committed to examining specifically how insurers’ claims handling arrangements drive good customer outcomes. A consultation planned for Q2 2026 will clarify responsibilities for claims outcomes across distribution chains — a direct challenge to the multi-organisation opacity at the heart of how PMI episodes are actually delivered.

The Consumer Duty’s four outcomes — products and services, price and value, consumer understanding, and consumer support — all require evidence at the level of the individual member’s actual experience of the product they purchased. For PMI, that product is funded clinical care. The evidence required is what happened during that funded care: which pathway was followed, who held clinical responsibility at each stage, whether the authorised treatment was delivered, and what the outcome was.

Population health evidence, however rigorous, does not answer an individual episode question. A peer-reviewed study showing 57% mortality reduction across an active membership base does not tell the FCA what happened to a specific member during the specific episode that insurer authorised and paid for. Those are different questions, and Consumer Duty requires answers to both.

Where the Prevention Model’s Evidence Stops

Vitality has published a comprehensive multi-part Consumer Duty framework covering fair value, good client outcomes, cross-cutting rules, foreseeable harm, and vulnerable customer support. It is thorough within its scope. That scope covers product design before care, engagement incentives before care, adviser quality measurement before care, and behavioural data before care.

The Prevention 2.0 thesis answers the fair value question with genuine authority — the product delivers value from day one through rewards, lower premiums for healthy behaviour, and access to the Vitality Programme. It answers the consumer understanding question through Distribution Quality Measurement data shared with adviser partners and detailed annual statement letters. It answers the foreseeable harm question through product design decisions — removing automatic mental health exclusions, adding Dementia and FrailCare Cover — that demonstrate genuine consideration of member needs.

What it does not address is the question the FCA is now specifically moving toward: what happened inside the funded episode? When a Vitality member is referred to a consultant under an authorised PMI pathway, moves through a diagnostic facility, undergoes a procedure at a private hospital, and is discharged to community follow-up — each of those transitions happens across a separate independent organisation. Vitality authorised the first step. What occurred at each subsequent handover is invisible until invoices arrive, which may be weeks or months after the episode has closed.

The episode-level evidence gap is not unique to Vitality. It is structural across the entire PMI market. But for an insurer whose commercial differentiation is built on the claim that structured data about health behaviour produces better outcomes, the absence of structured data from inside the episode itself is a specific and material asymmetry. The richest pre-episode intelligence model in UK insurance meets, at the point of clinical care, the same opacity as the most basic indemnity policy.

The AI Ambition and the Data It Needs

Vitality’s Google AI partnership and their genomics programme are investments in predictive intelligence — knowing which members are at elevated risk and supporting them to modify that risk before illness occurs. Their 2026 predictions name AI-enabled care pathways as a defining feature of the next era of private healthcare. That ambition is directionally correct and commercially astute.

AI-enabled care pathways, however, require data from inside care pathways. They require structured records of what clinical decisions were made at each stage of an episode, which service routing choices were taken, how responsibility transferred between providers, and what outcomes followed from which combinations of pathway decisions. Without that structured episode data, AI can optimise the journey to the practice door with considerable sophistication. It cannot optimise what happens beyond it.

The specific limitation is not computational — it is infrastructural. No PMI insurer currently captures structured clinical episode data at the point of inter-organisation handover. Episodes are reconstructed retrospectively from billing records, not recorded prospectively from clinical events. The data that AI-enabled pathway optimisation requires does not exist in the system that would use it. The Google partnership and the genomics investment are extending an intelligence model that will hit a structural ceiling at the exact point where its commercial and clinical value would be highest.

The Paterson Dimension

In February 2020, the Independent Inquiry into the issues raised by Ian Paterson found that his malpractice had been possible precisely because no structured mechanism existed to share information about a clinician’s practice across the multiple organisations in which they worked. Private hospitals granted practising privileges without accountability for what occurred under those privileges. Responsibility dissolved at each organisational boundary. The inquiry found not a failure of regulation but a failure of visibility — “our healthcare system does not lack regulation or regulators” — and called specifically for structured mechanisms to share clinical performance data across the independent sector, to record responsibility at each stage of a patient’s care, and to make that information visible to those who needed to act on it.

Five years on, clinicians who gave evidence to the inquiry still believe that “despite the changes, it was entirely possible that something similar could happen now.” The Medical Practitioners Assurance Framework has set standards for clinical governance in the independent sector. The structural infrastructure to make those standards operative across a multi-organisation episode — the mechanism that would make responsibility transfer visible and accountable at each handover point — has not been built.

For a PMI insurer, the Paterson question and the Consumer Duty question are the same question wearing different regulatory clothes. Both ask: what happened inside the funded episode? Both require a structured answer that the current architecture of private healthcare cannot produce.

What Completing the Model Requires

The Prevention 2.0 thesis is built on a conviction that structured data about health behaviour produces better outcomes. That conviction is correct. The peer-reviewed evidence supports it. The commercial model validates it. The natural extension of that thesis — the completion of the model — is structured data about clinical episodes producing better governed, better evidenced, better priced funded care.

Episode governance infrastructure built around structured identity, consent, provenance, clinical intent, responsibility transfer, service routing, and outcome recording does not replace the Prevention 2.0 model. It extends it into the domain where Prevention 2.0 currently goes silent. It produces the individual episode outcome evidence that Consumer Duty requires and the FCA is moving toward demanding specifically from PMI. It creates the structured episode dataset that AI-enabled pathway optimisation actually needs to function. It generates the provenance trail that answers the Paterson question about responsibility at each clinical handover. And it accumulates, over time, the outcome data by provider, condition, and pathway that makes value-based contracting possible — paying the providers who deliver the best outcomes more, and directing more members to them.

The insurer whose Prevention 2.0 model is completed by episode governance infrastructure can make a claim that no other insurer in the market can currently make: that their data about member health is continuous from first engagement through to clinical outcome, structured at every stage, and evidenced at the individual level that Consumer Duty requires and clinical governance demands.

That is not a compliance argument. It is the completion of the most commercially compelling thesis in UK private health insurance.

The Competitive Position

The episode evidence gap is uniform across the PMI market. Every insurer authorises episodes they cannot see. The FCA has confirmed this across the insurance sector and is moving specifically toward PMI claims handling with its 2026 review. The Paterson Inquiry’s unresolved structural recommendations have made it a patient safety governance obligation as well as a regulatory compliance requirement.

The first insurer to close the gap holds a position that cannot be replicated through product innovation, engagement programmes, or AI partnerships alone. They can evidence individual member outcomes at episode level to the FCA. They can present structured clinical governance data to employer scheme clients at renewal. They can demonstrate to the broker market that their directional care pathways actually direct in real time, not retrospectively. They can answer FOS complaints with an immutable structured record of what happened during the funded episode, not a reconstruction from fragmented billing data across six independent organisations.

Prevention 2.0 is the right model for PMI’s future. The episode is where that future needs to be completed.